Economics

Basic concepts of economics and allocations of resources

Scarcity

Human wants are unlimited but resources are limited and those resources are supplied in less amount than the demand. It is known as Scarcity.

Choice

Choice refers to the ability of a consumer or producer to decide which good, service, or resource to purchase or provide from a range of possible options.

Q NO.1 Scarcity is the central problem of the economy. Justify this statement.

Human wants are unlimited, but the resources are limited and those resources are supplied in less amount than the demand. It is known as Scarcity.

Scarcity is the central problem of the economy because while resources are limited, we are living in a society with unlimited wants. Therefore we have to choose. We have to make trade-offs. We have to effectively allocate resources. We have to do these things because resources are limited and cannot meet our own unlimited demands. People are creating unlimited demands, but there is less supply than demand so, that’s why scarcity is the central problem of the economy. People have a choice to choose the resources which are available.

In conclusion, Scarcity is the main problem of the economy because we have to choose the limited resources over the unlimited wants.

Production Possibility Curve

Introduction

Human wants are unlimited but resources are available to fulfill those wants are limited, they have alternative uses. The production possibility curve is also known as the production frontier curve or the production boundary curve to the production transformation curve.

Statement

Production possibility curve refers to locus focus of various alternative combinations of two commodities that can be produced utilizing the available means and resources and given technology by an economy in a certain time period

Assumptions

- The economy is producing only two goods.

- There is full employment of resources.

- Production technology is given and constant.

- The factor of production is given and constant.

- The time period is given.

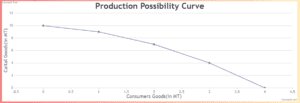

Table

| Combinations | Consumer goods | Capital goods | Opportunity Cost |

|---|---|---|---|

| A | 0 | 10 | – |

| B | 1 | 9 | -1:1 |

| C | 2 | 7 | -2:1 |

| D | 3 | 4 | -3:1 |

| E | 4 | 0 | -4:1 |

This table shows combinations, consumer goods, capital goods, opportunity cost. Here, combination A(0, 10) shows 0 MT consumer goods and 10 MT capital goods. Combination B (1,9) shows 1 MT consumer goods and 9 MT capital goods. Combination C (2, 7) shows 2 MT consumer goods and 7 MT capital goods. Combination D(3, 4) shows 3 MT consumer goods and 4 MT capital goods. Combination E(4, 0) shows 4 MT consumer goods and 0 MT capital goods.

Diagram

This figure shows that the x-axis measures consumer goods and the y-axis measures capital goods. In order to increase the production of one unit, more and more units of other goods have to be sacrificed since the resources are limited and are not equally efficient in the production of both the goods.

Conclusion

Hence, the resources are limited in order to increase the production of one good to the producer should have to sacrifice the production of other goods. The more unit of one commodity the more sacrifice of another commodity.

The shift in the PPC curve

The movement of the entire PPC form from its initial position to an inward or outward position, due to various reasons is called a shift in the PPC curve.

A rightward shift in the PPC curve

If the PPC curve moves upward due to technological progress, the discovery of natural resources, increase in the productivity of human resources, increase in the capital investment and increase in the capital formation, increase in the size of the population, etc is known as a rightward shift in the PPC curve.

Reasons for a rightward shift in PPC curve

- Due to technological change.

- Due to discoveries of natural resources in larger quantities.

- Due to the increase in the productivity of labor.

- Due to the increase in investment in capital and the increase in capital formation.

- Due to the increase in the size of the population.

A leftward shift in the PPC curve

If the PPC curve moves backward or inward due to the backwardness in technology, shortage of natural resources, lack of capital investment, lack of machinery, lack of skilled human resources, decrease in size of the population, migration, etc is known as a leftward shift in PPC curve.

Reasons for a leftward shift in the PPC curve

- Due to the backwardness in technology.

- Due to the shortage of natural resources

- Due to the lack of training for the labor.

- Due to the decrease in capital investment.

- Due to the decrease in the size of the population.

Division of labor

Dividing a whole task into different tasks and sub-tasks and done by separate labor according to skills, efficiency, and talent, etc is called division of labor.

Types of labor

1. Simple division of labor

If a task or work is entirely completed by a group of person then it will be known as a simple division of labor.

2. Occupational division of labor

If the people are categorized into various occupational groups like farmers, teachers, carpenters, etc then it is known as occupational division of labor.

3. Complex division of labor

Dividing a whole task into different tasks and sub-tasks and done by separate labor according to skills, efficiency, and talent, etc is called complex division of labor.

4. Territorial or Geographical division of labor

If some part of the country is specializing in the production of some goods it is known as territorial or geographical division of labor.

The advantages of the division of labor

- The right person is in right place.

- Increase in production.

- Optimum use of machinery.

- Saving of time.

- Development of skills.

- Production of quality goods and services.

- Possibility of increase in innovation.

The disadvantages of the division of labor

- The monotony of work.

- Loss of resposibility.

- Limited skills.

- Workers become dependent.

- Possibility of unemployment.

- Possibility of over-production.

- Possibility of decrease in productivity.

Specialization of labor.

The process of concentrating on and becoming an expert in a particular field, subject, or skills is a specialization of labor.

Advantage specialization of labor.

- Specialization in a particular task, the small job allows workers to focus on the part of the production process so they will be better at some jobs than at others.

- Workers who specialize in certain tasks often learn to produce quickly and with higher quality.

- Specialization allows businesses to take the advantage of economies of scale, which means that increases the level of output and decreases the average cost of individual units.

- Specialization of labor allows for big problems to be tackled with the efforts of many laborers.

Economic system

Economy is the system or the set of all activities related to production, consumption, and trade of goods and services in an area.

Types of economy

There are three types of economy. They are:-

- Market economy.

- Socialist economy.

- Mixed economy.

1. Market economy

The market economy is also known as a capitalist economy or free enterprise economy. In a market economy, all economic activities like production, consumption, distribution, exchange, etc are organized and carried out by private sectors and guided by profit motive through the market forces – demand and supply.

Market forces determine what to produce, how to produce, and whom to produce. Demand or supply of resources determines their respective share in total income. Similarly, demand for and supply of goods and services determine the equilibrium price and quantity in the market. There is no extra tax or subsidy on goods and services. Consumers are free to decide their consumption or saving. There is no control over consumption level from the side of the government. Individuals can conduct international trade themselves. There is no control over export and import. The private sector is the backbone of economic development.

Hence, Government is the monitor and supervisor of the economy, US, UK, Japan, Germany are the example of a market economy.

Features of market economy

- Economic activities are carried out by private sectors.

- Existence of market mechanisms.

- Consumer’s right.

- Limited role of government.

- Right of private property.

- Self-interest.

- No private monopoly.

- Class conflict.

The advantages of the market economy.

- Freedom of consumer.

- Mobility of factor of production.

- Efficient allocation of resources.

- Perfect competition.

- Technological innovation.

The disadvantages of the market economy.

- Creates economic inequality.

- Private sector domination.

- Profit motive.

- Possibility of illegal trade.

- Possibility of production and consumption of harmful goods.

- Neglects the production of public welfare goods.

2. Socialist economy

An economy in which all the economic activities are carried out by the central government for public welfare is called a command economy. A socialist economy is also known as a controlled economy or planned economy. In a socialist economy, resources are controlled by the state or government through the central planner.

In a socialist economy, all the wages, rent, interests, and profit are fixed by the government. The government decides what to produce, how to produce, and whom to produce. There is no existence of private property. In this economy, people are not guided by self-interest. They are guided by the interest of the nation. All the prices are set by the government since there is no private sector.

Hence, consumers are not free to choose goods and services for consumption. The government manages all economic activities. Some of the examples of socialist economies are North Korea, China, and the Former Soviet Union.

Features of a socialist economy

- Public ownership of factor of production.

- Social welfare.

- No existence of market mechanisms.

- Government has the absolute right to decision-making.

- No existence of private sector.

- No choice of the consumer.

- Economic equality.

- Class conflict.

Advantage of a socialist economy

- Equal distribution of income.

- Optimum use of all the resources.

- Social welfare.

- Long-term growth of the economy.

- Better national security.

Disadvantage of a socialist economy

- Barriers to the private sector.

- Lack of competitiveness in the economy.

- No consumers right.

- Possibility of misuse of resources.

- Lack of freedom.

3. Mixed economy

An economy in which economic activities are partly conducted by the government and private sector is called a mixed economy.

A mixed economy consists of both features of a socialist economy as well as a capitalist economy. Both government and private sector work together in this mixed economy. Major roles of the government are: providing security, supplying money, maintaining law and order, developing infrastructure, and so on. The private sectors are free to do their activities under the rules and regulations of the government.

Hence, production and distribution are managed and controlled by private sectors for the purpose of self-interest and profit earnings. The government sector prepares and implements policy instruments to control and regulate private enterprises directly and indirectly. Some of the examples of mixed economies are Nepal, India, Pakistan, Bangladesh, etc.

Feature of a mixed economy

- Public-private ownership.

- The majority of the economic activities are organized and carried out by the private sector.

- Government plays the role of facilitator.

- Consumers freedom.

- Better allocation of resources by a public-private partnership.

- Limited government intervention.

- Price mechanisms and controlled price.

- Profit motive and social welfare.

Advantage of mixed economy

- The private sector is guided by the profit motive and self-interest.

- Freedom and human rights.

- Relatively equal distribution of income and optimum use of resources.

- Check and balance by the government.

- The government provides basic necessities like water, electricity, telephone, etc.

Disadvantage of a mixed economy

- Possibility of high corruption.

- The economy may be dominated by the big private sector.

- Unwanted competition between private and public businesses.

- Delay in decision-making by the government

Market and Revenue Curves

Market

A market is a place or process where buying and selling of goods and services take place.

Classification of Market

1) Perfect Competition Market

A market system in which a large number of sellers sell a homogeneous product to a large number of consumers

is known as perfect competition.

Features

- There are a plenty of buyers and sellers.

- All the firms in this market sale the homogenous product.

- There is free entry and exit of firms.

- There is free mobility of the factor of production.

- The objective of the firm is profit maximization.

- The market is completely understood by both buyers and sellers.

2) Monopoly Market

Monopoly is a market system in which there is only one product supplier and a high number of customers.

Features

- There are a lot of buyers and just one seller.

- There are no close substitutes or items available on the market.

- There is a strong barrier to enter the new firms into the industry.

- Monopoly firms are called price maker.

- The profit motive is the firm’s goal.

- Monopolists use a pricing discrimination policy.

3) Imperfect Competition Market

I) Duopoly

Duopoly refers to market arrangements in which there are only two sellers of a product.

II) Oligopoly

Oligopoly is a market in which there are few sellers and numerous customers.

III) Monopolistic Competition

The market structure in which a big number of sellers sell differentiated heterogeneous items to a large

number of consumers is referred to as monopolistic competition.

Revenue

Revenue is the monetary value obtained by a company or industry through the selling of goods and services.

Total Revenue

Total revenue is the total amount of sales receipts or money value collected by a business or industry from

the sale of varied amounts of goods within a certain time period.

Average Revenue

The average revenue of a product is the revenue per unit of a product. The ratio of total revenue to quantity

is known as average revenue.

Marginal Revenue

Marginal revenue is the additional income received by a company or industry by selling one more unit of

production. Marginal revenue is defined as the ratio of change in total revenue to change in quantity.

Nature under perfect competition market

- TR rises at a constant rate in a perfect competitive market since the product’s price remains constant.

- In a market with perfect competition, MR remains constant.

- In a market with perfect competition, AR remains constant.

Nature under monopoly market

- In a monopolistic market, TR first grows at a decreasing rate, then reaches a maximum and begins to fall as

the price of the commodity falls as the selling amount increases. - MR stays constant in a monopolistic market.

- In a monopolistic market, AR falls as the price of products and services rises. AR can never be 0 or

negative.

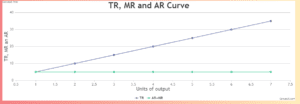

TR, MR and AR curve under perfect competition market

Table

| Units | Price | TR | AR | MR |

|---|---|---|---|---|

| 1 | 5 | 5 | 5 | 5 |

| 2 | 5 | 10 | 5 | 5 |

| 3 | 5 | 15 | 5 | 5 |

| 4 | 5 | 20 | 5 | 5 |

| 5 | 5 | 25 | 5 | 5 |

| 6 | 5 | 30 | 5 | 5 |

| 7 | 5 | 35 | 5 | 5 |

The units of several commodities are shown in the table above. The table also displays the price, TR, MR, and

AR. In a perfect competitive market, the commodity price remains constant. TR is the product of the price and

the number of units. TR and units are averaged to form AR. The MR is the ratio of the change in TR to the

change in quantity.

Diagram

The y-axis in the above table represents TR, MR, and AR, while the x-axis represents the units of output. In

this case, TR increases at a constant rate while MR and AR stay constant.

Relationship between TR, AR, and MR under perfect competition market

- TR rises at the same rate as AR or MR at all levels of sales. It specifies that TR, AR, and MR are all equal

for the first unit of sale. - For all levels of sales, AR and MR are equal and consistent.

- AR and MR are equivalent to the price.

TR, MR and AR curve under monopoly market

Table

| Units | Price | TR | MR | AR |

|---|---|---|---|---|

| 1 | 10 | 10 | 10 | 10 |

| 2 | 9 | 18 | 8 | 9 |

| 3 | 8 | 24 | 6 | 8 |

| 4 | 7 | 28 | 4 | 7 |

| 5 | 6 | 30 | 2 | 6 |

| 6 | 5 | 30 | 0 | 5 |

| 7 | 4 | 28 | -2 | 4 |

The above table shows the units of many commodities. The pricing, Total Revenue (TR), Marginal Revenue (MR),

and Average Revenue (AR) are also included in this table (AR). In a monopolistic market, the price of a

commodity declines. Total Revenue (TR) is calculated as the total of price and unit sales. Average Revenue is

calculated by dividing Total Revenue (TR) by the number of units sold (AR). The ratio of the change in Total

Revenue(TR) to the change in quantity is known as the margin of revenue (MR).

Diagram

The y-axis in the following table indicates Total Revenue (TR), Marginal Revenue (MR), and Average

Revenue(AR), while the x-axis represents the units of output. Total Revenue (TR) rises at a decreasing rate

until it reaches its maximum and begins to drop, whereas Average Revenue (AR) decreases but never becomes 0

and Marginal Revenue (MR) not only decreases but also becomes 0 and negative.

Relationship between TR and MR under monopoly market

- When TR increases at decreasing rate MR is positive.

- When MR becomes zero, TR reaches at its maximum.

- When MR becomes negative, TR starts to decrease.

- The decreasing and increasing rate of TR is equal to MR.

Relationship between AR and MR under monopoly market

- AR and MR have positive relationship. A decrease in MR cause to decline in AR.

- The decrease in MR is greater than the decrease in AR.

- MR might be negative; however, AR always remains positive.

- MR curve lies below the AR curve and halfway on the perpendiculars drawn from AR to the y-axis.

Numerical Problems.

1. a) Considered the following table.

| Units | Price | TR | MR | AR |

|---|---|---|---|---|

| 1 | 10 | 10 | 10 | 10 |

| 2 | 8 | 16 | 6 | 8 |

| 3 | 6 | 18 | 2 | 6 |

| 4 | 4 | 16 | -2 | 4 |

| 5 | 2 | 10 | -6 | 2 |

b) What types of market is this?

This is a monopoly market.

Diagram

2. a) Considered the following table.

| Units | Price | TR | MR | AR |

|---|---|---|---|---|

| 1 | 20 | 20 | 20 | 20 |

| 2 | 20 | 40 | 20 | 20 |

| 3 | 20 | 60 | 20 | 20 |

| 4 | 20 | 80 | 20 | 20 |

| 5 | 20 | 100 | 20 | 20 |

b) What types of market is this? Why?

This is a Perfect Competition Market because price remains constant in perfect competiotion

market.

c) Diagram

3. a) You are given following table:

| Units | Price | TR | MR | AR |

|---|---|---|---|---|

| 1 | 10 | 10 | 10 | 10 |

| 2 | 10 | 20 | 10 | 10 |

| 3 | 10 | 30 | 10 | 10 |

| 4 | 10 | 40 | 10 | 10 |

| 5 | 10 | 50 | 10 | 10 |

| 6 | 10 | 60 | 10 | 10 |

| 7 | 10 | 70 | 10 | 10 |

b) Plot TR, MR and AR in Graph

c) What type of market is this?

This is a perfect competition market.

d) What is the nature of TR curve?

TR curve increases at constant rate.

4. a) Consider the following table:

| Units | Price | TR | MR | AR |

|---|---|---|---|---|

| 1 | 10 | 10 | 10 | 10 |

| 2 | 9 | 18 | 8 | 9 |

| 3 | 8 | 24 | 6 | 8 |

| 4 | 7 | 28 | 4 | 7 |

| 5 | 6 | 30 | 2 | 6 |

| 6 | 5 | 30 | 0 | 5 |

| 7 | 4 | 28 | -2 | 4 |

b) Plot TR, MR and AR in Graph

c) What type of market is this?

This is a monopoly market.

Cost and Cost Curves

Basic concept of Cost

Cost

The sum of the price paid to the inputs like rent, interest, wages, and other by producer to produce goods and services is known as cost

1. Money cost

The value of payment made in terms of money to the inputs used in the production in the form of rent, wages, salaries, allowences, profit, interest and price of raw materials is known as money cost.

2. Real cost

Real cost is a sacrifice made by the producer while producing goods and services. For example, Discomfort, pain are some examples of real cost.

3. Accounting cost

Cost which are necessary for accounting purposes is known as accounting cost.

4. Explict cost

The monetary payment of cash expenditure which a firm makes to those inputs which are not owned by the firm itself are called explict cost.

5. Implict cost

Implict cost ia the contribution made by the producer and his/her family members but not paid to them in monetary terms.

6. Economic cost

Economic cost is the aggregate of explict cost and implict cost.

Economic cost = Explict cost + Implict cost

Short-Run cost

Short-run is a time interval, which is too short to change all factor of production. It means all factor of production are not variable in short-run. Some factors are fixed and some are variable. Cost incurred on both fixed and variable factor of production in the short-run is known as short run cost.

Fixed cost

The cost incurred on the fixed factor used in the process of production is known as fixed cost. In other words, fixed cost are those cost which in total do not change with any changes in output.

Variable cost

Variable cost is the cost incurred on the purchase of variable factors used in the production. In other words, variable cost are those cost which vary directly with production.

Total cost

The overall amount of cost incurred by the producer while producing various units of goods and services in given time period is called total cost.

i.e. TC = TVC + TVC

Marginal cost

Marginal cost is the additional cost on total added by the production of one more unit of output.

Marginal cost is defined as the change in total cost resulting from one unit change in the level of output produced.

Mathematically,

MCn = TCn – TCn-1

Average cost

Average cost is per unit cost of production. Average cost, at each level of output is calculated by dividing total cost by the corresponding level of output/production. Mathematically,

AC =

Short-Run Total cost

1. Total Fixed cost (TFC)

The total amount of cost incurred on the fixed factor in short-run in the production process is known as total fixed cost. The total fixed cost remains constant whatever be the level of output, i.e. zero or more.

2. Total Variable cost (TVC)

The total amount of cost incurred on the variable factors in short-run is known as total variable cost. TVC remains at zero at zero level of output and it increases with increase in output.

3. Total cost (TC)

Total cost is self-defining. It is the sum of total fixed cost and total variable cost at each level of output or production.

Therefore,

TC = TFC + TVC

Table

| Quantity | TFC | TVC | TC |

|---|---|---|---|

| 0 | 10 | 0 | 10 |

| 1 | 10 | 10 | 20 |

| 2 | 10 | 18 | 28 |

| 3 | 10 | 24 | 34 |

| 4 | 10 | 28 | 38 |

| 5 | 10 | 34 | 44 |

| 6 | 10 | 42 | 52 |

| 7 | 10 | 52 | 62 |

Diagram

Nature

- TFC remains the same whatever the output level, so TFC curve will parallel to x-axis.

- TC and TVC always have inverse s-shape due to the apply of law of variable proportion.

- TVC and TC curves are parallel to each other because the gap between TVC and TC is TFC which remains constant.

1. Average Fixed cost

- Average fixed cost is the outcome of total fixed cost divided by the unit of a commodity.

- Average fixed cost is the per unit fixed cost of the output.

- Average fixed cost goes on decreasing with the increase in output level but it is always positive.

- Average fixed cost takes the shape of L.

Mathematically,

AFC =

2. Average Variable cost

- Average variable cost is the outcome of total variable cost divided by the level of output.

i.e. AVC =

- At first, AVC decreases then reaches at maximum point and starts to increase.

- It takes the shape of U.

3. Average cost

- Average cost is the outcome of total cost divided by the level of output.

i.e. AC =

- AC is the summation of Average Fixed Cost and Average variable cost.

- Average cost is the per unit cost of the output.

- At first, AC decreases, then reaches at maximum point and starts to increase.

- It takes the shape of U.

Table

| Quantity | TFC | TVC | AVC | AFC | AC |

|---|---|---|---|---|---|

| 1 | 15 | 25 | 25 | 20 | 45 |

| 2 | 15 | 40 | 20 | 10 | 30 |

| 3 | 15 | 45 | 15 | 6.67 | 21.67 |

| 4 | 15 | 56 | 14 | 5 | 19 |

| 5 | 15 | 75 | 15 | 4 | 19 |

| 6 | 15 | 120 | 20 | 3.33 | 23.33 |

| 7 | 15 | 175 | 25 | 2.85 | 27.85 |

In this above table it shows units, average variable cost, average fixed cost, average cost, total cost and total variable cost where TFC is constant while TVC is increasing at decreasing rate and then it is increasing in increaing rate and AVC is determined by the TVC and units and AFC is determined by the TFC and units and AC is the sum of AVC and AFC.

Diagram

In this table, x-axis represents units y-axis represents AVC, AFC and AC and AVC takes the shape of U while AFC is taking the shape of english letter L.

Reason behind U-shaped AC curve/SAC curve

In the short run production process law of variable proportion operates. According to this law, At first, TP increases at increasing rate while TP of a firm increases at increasing rate. Total cost of firm increases at decreasing rate in this situation per unit production (AC) declines. So, At first SAC curve slopes downward after the certain output level TP increases at the decreasing rate in this situation total cost of the firm increases at the increasing rate and per unit cost also increases by this reason SAC slopes upward and takes the shape of English letter U.

Marginal Cost (MC)

- Change in total cost due to one unit change in output level is known as marginal cost.

- Marginal cost is the additional cost on total cost added by the production of one more unit of output.

i.e. MC = TCn – TCn-1

Table

| Units | TC | MC |

|---|---|---|

| 1 | 50 | 50 |

| 2 | 70 | 20 |

| 3 | 80 | 10 |

| 4 | 85 | 5 |

| 5 | 95 | 10 |

| 6 | 115 | 20 |

| 7 | 145 | 30 |

The given above table shows the units, total cost (TC) and marginal cost (MC). Here, TC first increasing at increasing rate then it is increasing at decreasing rate and MC is the change in TC.

Diagram

In this table, x-axis measures the units and y-axis measures the marginal cost. Marginal cost always takes the shape of U.

Relation between AC and MC curve

- When AC is decreasing MC lies below the AC.

- When AC is increasing MC lies above the AC.

- MC cuts AC from minimum point of AC.

- The decreasing and increasing rate of MC is faster than AC

Theory of price and output determination

Equilibrium

Equilibrium is a state of rest, where two opposing forces are in balance.

Equilibrium condition of the firm under TC-TR approach in perfect competition.

Please problem solve